Business

Specific Good Tax

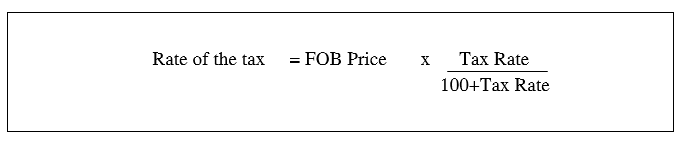

The following rate is described for the imported goods to local area.

If the Specific goods are locally produced, the specific goods tax shall be charged on whichever is higher, the sale price mentioned by the factory, workshop or workplace, or the sale price stipulated by the DG and the Executive Committee of the IRD based on the market price.

The following rate is described for the exported goods to abroad.

Commercial Tax

- The commercial tax shall be 5% on the sale price of products. If the products are the Specific Goods, commercial tax shall be charged on the sale proceeds including the specific good tax.

- The commercial tax shall be 3% on the sale proceeds of the building built and sold.

- The commercial tax shall be 1% on the sale proceeds of Golden Jewelleries.

Income Tax

- While calculating the income of the companies, the cost of goods, the expense to make the income and depreciation are deducted from sale proceeds exclusive of commercial tax. The income tax is 25% on the net profit after the deduction.

- If the companies have the capital gain from the alienation or the exchange or the transfer of one asset or more, income tax shall be paid at 10% in kyats or foreign currency. If they are foreign companies, 10% income tax shall be paid in the currency received.

(How to forecast the tax due is available in the Tax Calculator Link.)

- As a company operation in Myanmar Oil and gas sector, the income tax shall be paid on the capital gain according to the following tax rates in the currency received-

Gain Income tax rate to be charged

- Up to equivalent kyat millions (100,000) 40%

- From kyat millions (100,000) to (150,000) 45%

- Kyat millions (150,000) above 50%

Stamp Duty

In the case of the lease of capital assets such as land, building, motor vehicles and water vehicles, when the company rents or hires, the stamp duty shall be charged as follows: (The Burma Stamp Act: Schedule-1, No.35)

- Where the lease purports to be for a term of less than one year (one half percent on the whole amount of rental fee)

- Where the lease purports to be for a term of not less than one year but not more than three years (one half percent on the amount of average annual rent reserved)

- Where the lease purports to be for a term in excess of three years (two percent on the amount of average annual rent reserved)

- Where the lease does not purport to be for any definite term (two percent on the amount of the average annual rent which would be paid for the first ten years)

- Where the lease purports to be in perpetuity (two percent on one-fifth of the whole amount of the rents which would be paid in respect of first fifty years)

- The tax due shall be paid by the person who hires.